You will have a few options to consider if you are close to retirement.

Deferred retirement

- If you choose to defer your retirement, your savings will remain invested in the Funds until a later stage, when you decide to take your benefit (no later than age 75). This means that you will retire from your employer, but will remain in the Fund, until you decide what to do with your retirement benefit. You will also only pay the necessary tax on any cash lump sum you elect to take after you have made a decision.

- The administration fees that are due after the date of your actual retirement will be deducted monthly from your Fund Value. Usually, these fees are deducted from your contributions, but as you will no longer be contributing to the Fund, they will need to be deducted from your Fund Value instead.

- You will have to make an active investment choice, so you can no longer stay in the Life Stage portfolio. The same investment options, switching rules, and switching costs that apply to active members also apply to deferred retirees.

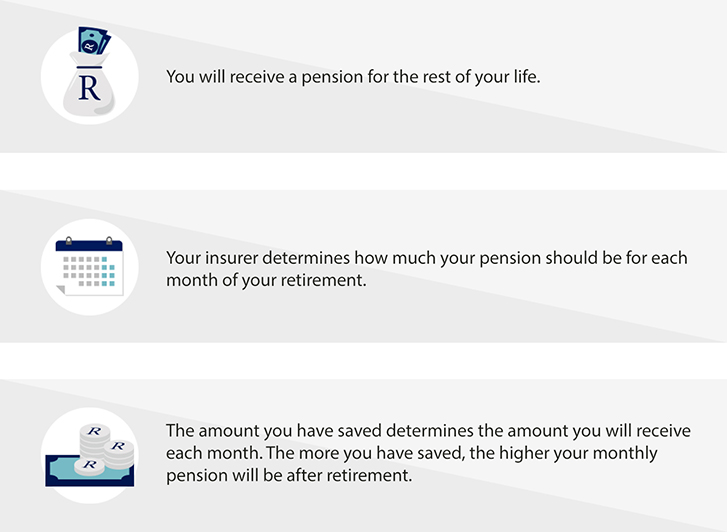

Guaranteed life annuity

Living annuity

Your monthly pension is guaranteed for life. | Your pension can be changed every year. |

The insurer will determine the investment strategy of the underlying investments. | The choice of underlying investments rests with you and your advisor. |

The insurer takes on the investment risk. Your monthly pension is guaranteed. | You take on the investment risk. Together with your advisor, you must ensure that your investment returns provide a pension that you will be able to live on for the rest of your life. |

Your choice is final and cannot be changed. | A Living Annuity can be switched to a Fixed Annuity at a later stage. |